AMP Deputy Chief Economist Diana Mousina examines the impact of slower Chinese economic growth on Australia

As economic growth in China shows signs of slowing down, how will this affect the Australian economy and investment markets? To find out, we looked at four areas of economic activity – overall exports, resources, tourism and education.

Overall exports – holding up

It’s commonly accepted that Australia is highly dependent on the Chinese economy because of demand for our mineral resources and agricultural products.

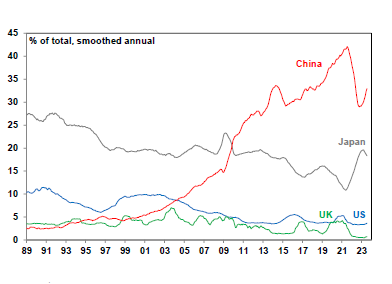

China has been Australia’s top trading partner since late 2009, as you can see in the chart below. Goods exports to China reached a peak of 42% in 2021 and have fallen since to 33%, due to:

trade tensions between Australia and China which impacted around $23billion worth of goods.

COVID-19 lockdown disruptions which reduced Chinese import demand

weaker Chinese growth.

Australian goods exports by destinations

Source: ABS, AMP

Source: ABS, AMP

But despite falling exports to China, Australia’s trade surplus is still averaging $11 billion over 2023 – that’s roughly double the level before COVID.

Resources – a mixed picture

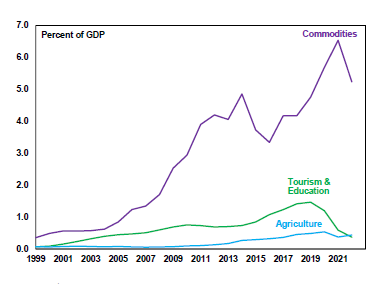

Commodity exports like iron ore, coal and Liquified Natural Gas are our main link to the Chinese economy and are worth over 5% of GDP to Australia, as you can see in the chart below. They benefited from strong economic growth in China in the decade before the pandemic.

Australian exports to China

Source: ABS, AMP

Source: ABS, AMP

Let’s look more closely at iron ore, which is Australia’s largest export, accounting for 22% of total exports. China uses iron ore to make steel for buildings, infrastructure and consumer products like electric vehicles.

The volume of iron ore exports has fallen to 8.5% from a peak of 10% in 2020. And although prices have remained high, demand could be further affected as Chinese economic growth slows to 4% over the next few years.

On the other hand, there are reasons to be optimistic.

China’s urbanisation has a way to go from its current level of 64% – this is well below advanced economies, which tend to be over 85%.

Australia is a high-quality producer of iron ore with less delays, strikes and closures than Brazil or the domestic Chinese market.

Other export markets like Japan, South Korea and Taiwan could absorb some of the slack from lower Chinese demand.

China’s economy is much bigger than 2006-10 when it was growing at 10%, so demand could be relatively unaffected.

The strength in commodity prices has helped improve Australian Government finances and is one reason we ended up with a Budget surplus of 0.9% of GDP in 2022-23.

This could give the Government room to lift spending, although this would probably be unwise at the moment due to high inflation.

Tourism – looking up

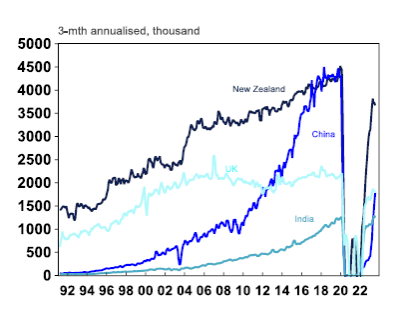

Before the pandemic, China (along with New Zealand) was the top source of short-term visitors to Australia, as you can see in the chart below. And they haven’t yet started to return in the same numbers – Chinese visitors are still less than half of their pre-pandemic levels. By comparison, overall visitor levels have recovered more and are only 30% below.

Short-term arrivals into Australia

Source: Macrobond, AMP

Source: Macrobond, AMP

But the impact on tourism has not been disastrous, as employment in areas like accommodation and food services, retail, and arts and recreation has held up well over the past year. The lack of Chinese short-term arrivals has been offset by high holiday spending by Australians and a high level of permanent migrants into Australia, with net overseas migration running around 500,000 or more – a record high.

Education – demand still high

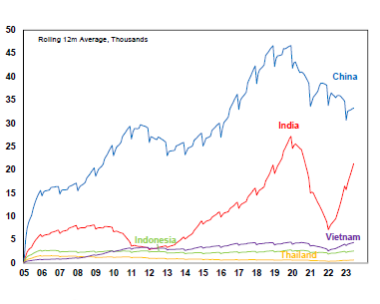

Chinese students have been the major country group of education arrivals into Australia since 2005. The pandemic has led to some drop-off, but the impact has not been as large as tourism which has helped to support the higher education sector – as you can see in the chart below.

Australia: Student Commencements in Higher Education

Source: Bloomberg, AMP

Source: Bloomberg, AMP

The outlook for China…

Chinese GDP growth is expected to fall over the next few years due to:

high debt levels

property oversupply

an aging population

slowing productivity growth.

This could result in world economic growth slowing from a long-term average of 3% to 2.5-2.7% a year.

…and what this means for investors

Lower Chinese demand for resources is one reason Australian shares have been close to flat throughout 2023 and underperformed the US and Europe, along with poorer earnings growth and households that are more sensitive to interest rate changes.

And concerns about the Chinese economy have partly led to the value of the Australian dollar falling by 6% since early 2023.

But overall our economy is showing enough flexibility to overcome weakness in Chinese economic growth. This means Australia may not be as reliant on China as many people think.

This article has been written by Diana Mousina, Deputy Chief Economist at AMP.

Important note: While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.